Modern IPOs are Victory Laps, Not Starting Lines

Public markets have historically been the arena where companies grew from promising upstarts into industry titans. Today's IPO isn't a beginning, it's an exit.

- 01The median tech company now IPOs at age 14 with $218M in revenue, vs. age 6 and $12M in 2000. Most exponential value creation now happens before the public listing.

- 02The "missing middle" of $100M to $500M revenue companies sits almost entirely in private markets, the historic sweet spot of risk-adjusted returns.

- 03Tactical, properly underwritten private secondaries are the cleanest entry into this growth segment.

Modern IPOs are Victory Laps, Not Starting Lines

Public markets have historically been the arena where companies grew from promising upstarts into industry titans. Investors could participate in this wealth creation journey from the beginning, riding the exponential growth curve all the way up. At least, that's how it used to work.

For technology firms, that model is dead. And investors who haven't adapted are missing the most lucrative phase of company growth cycles.

Today's IPO isn't a beginning—it's an exit. Companies delay public offerings until well past their prime growth phases, leaving public market-only investors without access to the most valuable segment of the growth curve. In short, this is a fundamental restructuring of capital markets that demands a strategic response.

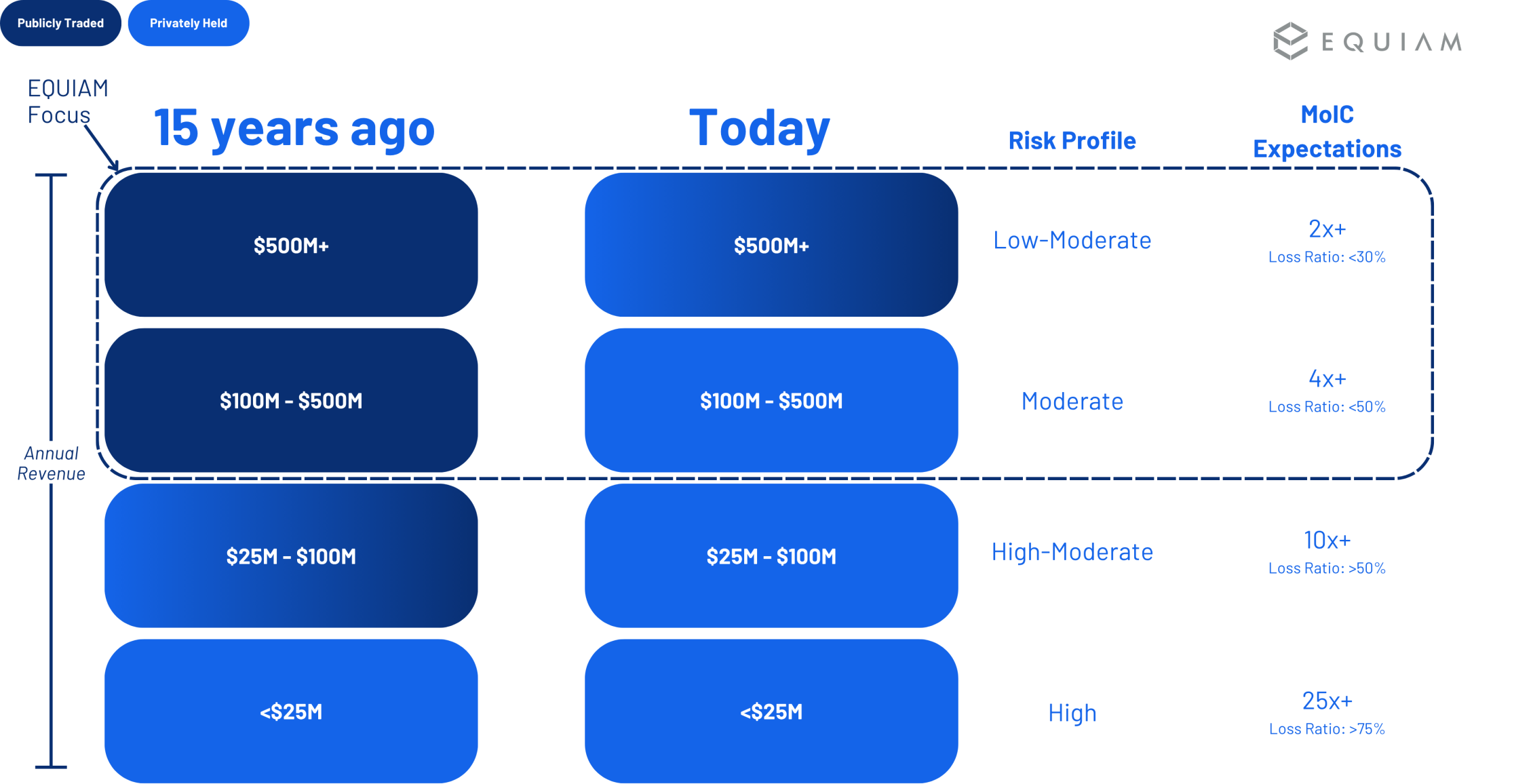

The Vanishing Middle

Public tech has become increasingly bifurcated. It's dominated by mega-cap behemoths on one end and companies that went public too early (often speculative and unprofitable) on the other. What's conspicuously missing? The sweet spot of high-quality, moderate-risk companies with $100M-$500M+ in revenue that historically delivered exceptional returns.

This "missing middle" represents the most attractive segment of the growth curve. These businesses have proven product-market fit, established revenue models, and sustainable unit economics—yet they remain locked in private markets because they can continuously raise private capital at favorable terms. The critical growth stages that transformed companies like Amazon, Microsoft, and Apple from promising startups into market dominators now occur almost entirely before IPO for today's winners.

Many investors are sitting on the sidelines during this crucial wealth creation phase, creating an existential threat to their long-term portfolio performance.

Tech Wealth Creation Happens Long before IPO Day

According to University of Florida research, the median age of tech companies at IPO has more than doubled from just 6 years in 2000 to 14 years in 2024. Even more dramatic is the revenue transformation. Companies once went public with median sales of merely $12 million (2000), compared to $217.9 million (2024). Case in point, the year before Amazon went public (1996), they generated revenue of $15.7M ($31M in 2024 dollars).

Most exponential valuation increases now occur in private markets. SpaceX has grown to $350 billion. ByteDance hit $300 billion. Stripe reached $91.5 billion. This massive valuation creation, formerly available in public markets, is now entirely private.

The Goldilocks Zone of Private Markets

This $100M-$500M+ revenue segment, pending entry price, represents the ideal balance between risk and reward—a "Goldilocks zone" in the investment landscape.

Early-stage venture capital with sub-$25M revenue companies offers lottery-ticket economics. Yes, the occasional 100x return makes headlines, but most investments fail completely. Correlation Ventures analyzed over 21,000 venture financings and found that 65% of venture investments fail to return initial capital, with only 4% delivering 10x or more. Harvard Business School research confirms this reality, revealing that approximately 75% of venture-backed companies never return capital to investors.

Large public companies offer stability but minimal growth. When companies finally IPO, they've typically hit the asymptotic part of their growth curve. You might get 15-20% annual growth if you're lucky, hardly the exponential returns that build significant wealth.

Private growth/late-stage companies occupy the perfect middle ground. These aren't speculative bets—they're proven businesses with established products, real revenues, and sustainable unit economics. Yet they still can deliver exceptional growth, creating tremendous value without the extreme risk profile of early-stage ventures.

These companies remain private by choice, not necessity. They can raise capital on favorable terms without subjecting themselves to quarterly earnings cycles. Many are already leaders in their respective subsectors, having outcompeted rivals and established defensible market positions.

The Secondary Market Access Angle

It's not groundbreaking advice to suggest someone should "buy great companies", but the second, often unsaid, part of that advice is "at fair prices". Overvaluation and froth are common when new venture rounds are priced in hotly desired growth-stage firms. These growth-stage primary rounds are rarely priced in a way that stands up to institutional-grade underwriting.

The private direct secondary market offers a compelling pathway to mitigate this issue. For investors who are willing to be patient, rigorously underwrite, and then proactively source supply via multiple channels, the secondary market offers an effective way of building a portfolio of excellent growth-stage companies at sensible prices.

Owning the Full Growth Curve

The growth segment has migrated almost entirely to private markets, and this structural shift isn't temporary.

The choice isn't between private and public markets—it's between participating in the full growth curve or only its later, flatter stages. Forward-thinking investors are recognizing this reality and adapting their strategies to ensure exposure to this critical slice of the market.

In this new landscape, those without a private market strategy aren't just missing opportunities—they're structurally disadvantaged in a way that compounds over time. And within private markets, tactical, properly underwritten secondary transactions may represent the most advantageous entry pathway.

Public markets aren't what they used to be. The most valuable growth segment has moved private.

Connect with Our Team

Interested in learning more about our investment approach?